Should you invest in DAC? Answer 3 questions to find out.

Build your own thesis by considering these key criteria.

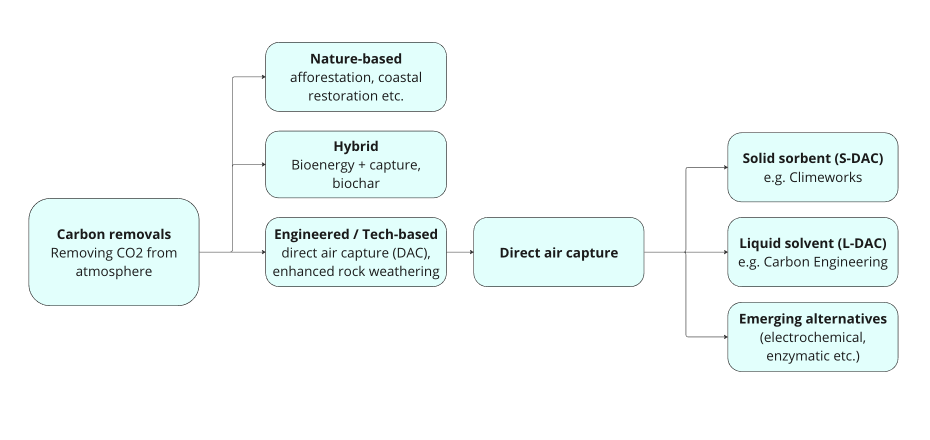

Start here: Do you believe in the need for carbon removals?

Option 1: YES, carbon removals are needed to address climate change and will be highly demanded by voluntary carbon markets.

Here are some reasons to believe, like we do at Revent, that carbon removals will be needed to hit climate targets:

In October 2018, the Intergovernmental Panel on Climate Change (IPCC) stated that “all analysed pathways limiting warming to 1.5°C with no or limited overshoot use carbon removal to some extent”, especially to address hard-to-abate emissions for which no viable mitigation measures have been identified.

There is growing demand from voluntary carbon markets for removal, rather than the currently predominant avoidance credits. While removal credits only accounted for an estimated <5% of voluntary carbon markets currently, BCG estimates that removal credits are expected to reach 35% by 2030.

Option 2: NO, we don’t need carbon removals to avoid climate disaster.

You’d have to believe that the world will suddenly and drastically lower emissions within the next five years to avoid overshooting the bounds for limiting global warming to 1.5°C. The scientific consensus is that this step change is very unlikely.

Alternatively, you’d have to be ok with exceeding 1.5°C of warming, and perhaps believe that adaptation will limit the consequences on human society.

If you chose YES, continue to the next question.

If you chose NO, you can stop here (but we’d urge you to reconsider).

Question #2: Do you believe that Direct Air Capture (DAC) is a vital class of carbon removals?

Option 1: YES, DAC will play a vital role in limiting global warming to 1.5°C, and DAC removal credits will be highly sought after by the voluntary carbon markets.

Some points towards the necessity of DAC include:

Land use: An Oxfam report found that, “Using afforestation alone to … achieve ‘net zero’ by 2050 would require at least 1.6 billion hectares of new forests - five times the size of India, and more than all the farmland on the planet.” A DAC facility, on the other hand, takes much less land per ton CO2 removed and can theoretically be sited anywhere, including non-arable land.

Removal quality: DAC combined with underground storage ensures much higher permanence (thousands of years) than nature-based solutions (decades). Furthermore, biomass is susceptible to wildfires, floods, and other carbon reversal risks.

Market demand: Companies with high Scope 3 emissions - especially in deeper-pocketed sectors such as tech, finance, and consulting - are voluntarily choosing to procure more DAC removals, despite their much higher cost, thanks to their ease of verification and permanence upon storage. Microsoft led the charge with their 2018 report detailing the importance of DAC in their removals portfolio.

Option 2: NO - DAC is controversial and limited by inherent thermodynamics. It will fall out of favor compared to other forms of carbon removal.

DAC has had its fair share of critics. Points they raise include:

Removing 400 ppm (trace amounts) of CO2 from the air comes with fundamental thermodynamic challenges, meaning that DAC will likely remain one of the most energy-intensive ways of removing atmospheric CO2.

Some, such as Stanford Professor Mark Jacobson, argue that rather than allocating our currently limited supply of cheap renewable energy towards DAC, it would be better for climate goals if the same green energy went towards replacing gas or coal.

DAC frontrunners such as Carbon Engineering and Global ThermoStat have received significant support from large oil companies, sparking concerns that DAC could be used justify continued fossil fuel use.

Other lower-cost removal options may come to dominate:

Nature-based solutions such as afforestation may overcome their verification and durability challenges (e.g. bioenergy with carbon capture & storage, biochar etc.) and become the predominant, trusted form of carbon removal, thanks to their affordability.

If you chose YES, follow us to the next question (we believe that it’s too early to eliminate any removal technologies from our arsenal against climate change).

If you chose NO, you can stop here.

Question #3: Do you believe that DAC players can bring costs down? And if so, will there be enough demand to drive mass scale-up of DAC?

Option 1: YES - at least one class of DAC technology should demonstrate exponential cost-down and scale-up in the next decade, bringing cost below $100/ton CO2 captured.

There are many emerging policy tailwinds for the scale-up of various DAC technologies:

Generous government support is enabling more mature technologies, like solid sorbents-based DAC (S-DAC) and liquid-based DAC (L-DAC), to break ground on a first round of commercial-scale projects.

Carbon prices in markets such as the EU are starting to approach the social cost of carbon, which is estimated to be over $100/ ton. Especially if accounting frameworks are standardized to favor permanence, or if cost of nature-based removals shoot upwards due to supply constraints, this could make the high price tag of DAC removals more palatable.

Renewables prices continue to fall, thanks to global decarbonization efforts. Meanwhile, breakthroughs in abundant clean energy baseloads (geothermal, maybe even nuclear fusion) seem to be on the horizon. All this bodes well for DAC’s energy-intensive opex.

Many companies are developing pathways to higher-value carbon utilization (e-fuels, chemicals etc.), rather than storage. This may unlock demand for DAC-sourced CO2 beyond just voluntary carbon markets.

A number of promising technical advances have also taken place:

Existing S-DAC and L-DAC approaches are both being demonstrated in first-of-a-kind large-scale projects - Climeworks is building a 36,000-ton S-DAC plant in Iceland, while Carbon Engineering has broken ground on a planned 500,000-ton/yr L-DAC plant in the US’s Permian Basin.

S-DAC should see faster learning rates because of its modularity and lower capex barrier to entry. This means many players can iterate on different approaches, and higher parts quantities enable economies of scale.

L-DAC may see significant cost-down dependent on the success of Carbon Engineering’s enormous plant, due to be operational by end of this year. Carbon Engineering has plans for dozens more plants to come.

In a model based on IEA Net Zero Scenario energy prices, both show potential for levelized cost of capture to approach ~$100/ton, compared to current cost of >$500/ton.

New DAC systems based on electrochemistry, biochemistry, and other mechanisms are being explored with hopes of drastically lower energy needs, and thereby lowering cost.

Option 2: NO - despite much investment and attention, the cost of DAC at scale is still too high compared to nature-based removals. DAC removals will remain a niche part of the voluntary carbon markets.

You might be discouraged after considering that:

Nature-based carbon removal credits currently cost $15-30/ton CO2 captured, much lower than even the long-term cost target of $100/ton cited by most direct air capture companies. As such, perhaps only the most deep-pocketed removals buyers (e.g. select tech companies and banks) will opt for DAC removals, while the bulk of demand remains for other types of removals.

In 2022, available DAC capacity was 0.01 Mt (10,000 tons) across 18 plants worldwide. In order to hit the IEA’s Net Zero target for 2030, capacity needs to triple every year until 2030. There may not be sufficient risk-tolerant growth and project capital to support this level of capex-heavy expansion of a technology & market has yet to be proven at scale.

The upstream (e.g. sorbent supply) and downstream (e.g. access to underground storage) need to be simultaneously developed along with core DAC technology - bottlenecks along the value chain may hinder scale-up.

If you chose YES, continue to the next question.

If you chose NO, you can stop here (and we’d understand - predicting the future of a technology is hard!).

So… you really believe in the future of DAC!

Bonus question: What kind of solutions should you look to support? What does “good” look like?

Here are a few different flavors of DAC companies we’ve seen, and our thoughts on what they’d need to succeed.

DAC Hyperscalers: Companies (e.g. CarbonCapture) who seek to plug the shortage of DAC removal projects, and believe that the rapid deployment of existing (usually S-DAC) technologies is the key to both market leadership and cost-down. As this approach is really all about ops and breakneck scaling, the team should be able to show:

Deep experience with project financing & development involving complex stakeholders

Proven track record of operational excellence

Access to / co-location with cheap, ideally renewable, energy

Access to / co-location with suitable CO2 permanent storage sites

A system design that is easy to scale out yet flexible enough to adapt to different operating conditions (climate, air quality, renewable energy availability etc.)

Strong partnerships with manufacturers of equipment and materials

Relationships with DAC removal buyers & brokerages, including deeper partnerships that involve project financing, long-term contracts etc.

Component Innovators: Companies (e.g. Global ThermoStat) improving upon core cost-driving components such as sorbents or contactors. Their team should have relevant expertise to develop a technology that:

Enables significantly lower capex, materials usage, and/or energy use than currently used S-DAC and L-DAC components

Is compatible with existing, scaled S-DAC or L-DAC infrastructure

Can be manufactured using existing equipment, processes, and service providers

Avoids relying on exotic or expensive raw materials

Systems Pioneers: Companies (e.g. RepAir) who are developing completely different mechanisms to mainstream S-DAC and L-DAC. Their team should have relevant expertise to develop a technology that:

Enables much lower cost in energy, materials and/or equipment than S-DAC and L-DAC systems

Shows favorable economics under a variety of conditions: climates, grid mixes, renewable energy availability etc.

Is based on equipment and materials supply chains that already exist at scale, perhaps transplanted from a different application area

Avoids relying on exotic or expensive raw materials

We hope this has been a useful exercise for you, as it has for the Revent team! We’d love to hear your thoughts - reach out at sharon@revent.vc or comment below.