Decarbonising Heavy Freight

How EV trucks will lead the charge

TL;DR

Road freight is responsible for nearly 75 percent of global freight emissions, according to BNEF. Within that, heavy-haul transport carries the largest share of road kilometres travelled (around half of UK freight), yet has historically received the least attention.

Only in the last few years has the industry landed on electrification as the credible pathway to decarbonise this segment. Battery electric trucks are now technically viable, and increasingly capable of delivering competitive economics across core use cases.

The scale of the transition ahead is enormous. There are just 10,000 battery electric trucks on European roads today, out of a 6.5 million strong fleet. A fully electric fleet would be around 2 terawatt hours of batteries and require charging infrastructure that spans all member states.

The good news is that the momentum is building. Tailwinds suggest this is a question of timing, not possibility. Electric trucks offer real advantages to drivers. Policy may wobble, but the overall direction remains one of pressure on diesel and support for zero-emission alternatives.

Where we go from here hinges on economics. If we can overcome the barriers around charging cost and infrastructure availability, electrification becomes a no-brainer for large fleet operators. Better total cost of ownership will drive adoption. Getting there won’t be easy, but the prize is large.

In what follows, we set out why electrification is inevitable, what is still holding it back, and where the biggest opportunities lie to build the next generation of climate-critical logistics companies. Strap-in, we’re gonna go deep.

Scroll to the bottom for the market map.

The opportunity of heavy goods decarbonisation

Road freight is not just the largest contributor to freight emissions, it is also the most entrenched. Within transport, it accounts for the highest share of emissions. Within freight, heavy goods vehicles (HGVs) dominate the emissions profile.

In the UK, HGVs are responsible for around 55 percent of all road freight emissions. Across the EU, there are approximately 6.5 million medium and heavy trucks on the road (ACEA), operating across a dense, cross-border network. The ten largest EU member states account for more than 80 percent of road freight volume, according to Upply.

Crucially, freight demand is not going away. The IRU projects that road freight volumes will continue to grow modestly through at least 2026. This is not a sector in structural decline.

That creates a sharp challenge. Emissions must fall rapidly from today’s levels to align with net zero targets, yet the volume of goods transported by road is expected to increase. This is the essence of the decarbonisation challenge, the underlying activity is growing, not shrinking. A successful transition here unlocks an enormous climate dividend.

Before we dive further into the tailwinds, barriers and opportunities to transform this sector, we need to understand some basics about how the road freight industry works.

Road Freight 101

Road freight is the backbone of the European logistics system. It covers the full spectrum of activity, from raw materials moving into factories, to finished goods being delivered to customers. Each year, EU roads carry over 13 billion tonnes of goods, with food and drink representing the single largest category at around 17 percent of total volume (Eurostat, 2023).

The sector is structured along a few key dimensions, simplified as:

Distance: long-haul, mid-haul, and last-mile

Vehicle type: light, medium and heavy-duty trucks

Vehicle use: from refrigerated to curtain-sided, box-bodied, tipper, flatbed, and tankers

This deep dive focuses on heavy goods vehicles. There are two simple reasons for that. First, HGVs are responsible for the majority of emissions within the road freight system. In the UK, for example, they account for around half of all kilometres driven by freight vehicles. Second, this is the segment that has seen the least progress to date. Electrification of smaller vehicles is already well underway. HGVs are the last frontier.

The contrast is striking. At the lighter end of the spectrum, the shift to electric is happening quickly. In many major cities, 40 to 50 percent of local deliveries are already made using electric vehicles. DPD in the UK is now operating with a fleet that is 40 percent electric (dashboard). Within London’s congestion zone, Amazon has reached 70 percent electrification. These transitions have largely gone unnoticed by end customers.

When averaged across the globe we see the EV share of sales in the light commercial vehicle segment at around 10 percent (BNEF EV Outlook, 2025). Buses offer another case study. In China, electric buses account for more than 95 percent of the urban fleet, and even in emerging markets, electric buses have started to dominate where the economics work.

The Value Chain

The value chain of road freight is made up of three core segments; starting with the vehicle and input manufacturers, through to the logistics operators (i.e. those operating the truck networks) and finally the end shipment demand (whether directly from shippers, or via aggregators). The figure below shows the flow of goods/services between the key segments in an electrified truck scenario.

This is important context, because it highlights that the transition in driving technology is NOT only a primary concern for the truck & trailer OEMs, but instead is a big disruptor for the operations that enable logistics service providers to run their truck networks, and it is these operations that must help to unlock the economics of BEV heavy duty trucks at scale.

Focusing Squarely on Electrification

Electrification has emerged as the only viable pathway to fully decarbonise heavy-duty road freight at scale (besides Hydrogen for very niche use cases). Other technologies (hybrid, HVO) play supporting roles, but only battery electric vehicles can deliver the depth of emissions reductions required to meet net zero targets.

The industry did not reach this conclusion overnight. The earliest efforts to decarbonise road freight focused on minimal disruption. Dual-fuel configurations, compressed and liquefied natural gas, hybrid drivetrains, and hydrotreated vegetable oil were seen as lower-friction solutions. These options preserved existing vehicle architecture and refuelling infrastructure.

But the regulatory bar kept rising. European emissions targets required steep reductions in tailpipe CO₂ that hybrid or biofuel-based approaches simply could not deliver. In parallel, regulators clarified that HVO use would not count towards manufacturer compliance, undercutting the incentive to adopt.

Attention turned to battery electric and hydrogen. For some time, hydrogen was seen as the more plausible route for long-haul freight. It offered faster refuelling and the prospect of a better range than BEVs. But as the technical details came into focus, the drawbacks of hydrogen became clearer. Fuel cell systems are far less energy efficient than batteries. The range advantages were overstated. And crucially, unlike batteries, there is no headroom to improve the energy density of hydrogen. Several OEMs that had invested heavily in hydrogen shifted their focus quietly but decisively.

The realisation that battery electric trucks were not just possible, but viable, began to take hold around 2021/2022. Early models like the Daimler FUSO eCanter (lighter truck) which came in 2017, followed by the Tesla Semi (HGV) in 2022 challenged the assumption that long-haul electrification was out of reach. Over the next two years, the performance of battery electric trucks in real-world conditions accelerated that shift in thinking.

Marginal abatement cost studies, which assess decarbonisation options based on emissions impact and cost, consistently rank battery electric trucks as essential to reaching deep emissions cuts across all segments. No other technology delivers more than modest reductions in the long-haul category. The UK Government compiled a comprehensive overview of available options in its Future of Mobility review, confirming that electrification is central to any high-ambition pathway (UK Gov, 2019).

Despite this growing clarity, adoption remains in the early stages. There are only around 10,000 battery electric trucks on the road in the EU, out of a total fleet of 6.5 million. Uptake has so far concentrated in markets where charging infrastructure is more mature and operating subsidies are in place. In California, for example, operators are already achieving cost parity on select routes. Diesel truck registrations in Europe fell by 16 percent between early 2024 and 2025, while electric truck registrations increased by 51 percent, reaching 3 to 4 percent of new vehicle sales (Upply and IRU, 2025).

We are also seeing a broadening of the manufacturer base. What began with beachhead products like the Tesla Semi has now expanded to include established European OEMs with full EV order books, as well as aggressive new entrants. Chinese manufacturers such as BYD, Farizon and Windrose are pushing prices down and accelerating production timelines.

The latest BNEF EV outlook (2025) shows that electrification is now moving into all segments of road transport, and we anticipate quite a sharp rise in EV share sales in the medium and heavy - haul truck segment in the coming 5 years. They also found no viable scenario where the 2018 peak in ICE sales would be returned to.

We believe the shift is no longer in doubt. The open question is timing.

Tailwinds

The scale of the transition is clear. We will need to electrify 6.5 million medium and heavy-duty trucks across Europe. In most regions, the total cost of ownership for electric HGVs is still not favourable compared to diesel or HVO alternatives. In short, there are real barriers to scaling.

Unlike personal vehicles, commercial fleet decisions are tightly linked to cost. This makes total cost of ownership the decisive factor. We explore the key cost barriers later in this article.

First, though, it is worth acknowledging the tailwinds. These point to a transition that is not a matter of if, but when.

Tailwind #1 Operational Advantage

Battery electric trucks are expected to outlast their diesel counterparts in total kilometres travelled. We already see this dynamic in the passenger vehicle market, where electric cars are logging longer lifespans than petrol vehicles, and are closing in on diesel (Nature, 2025). The data is more limited on HGVs, and so this hypothesis is to be proven, but generally speaking BEVs are less sensitive to usage intensity, given they tend to have fewer moving parts and battery degradation is typically more predictable than the degradation of a petrol/diesel engine.

Electric trucks also offer a materially better driving experience. Instant torque makes them more responsive. Noise and vibration levels are significantly lower. We believe these are not trivial benefits, they matter to drivers, spending days on end on the road. With appropriate range and charging access, we believe driver preference will shift decisively toward electric cabs.

In some jurisdictions, we are already seeing regulatory benefits tied to this improved performance. Electric HGVs are quieter, cleaner, and emit no tailpipe pollutants, which allows them to operate with fewer restrictions in sensitive zones. These dynamics are already evident in the lighter vehicle segment, where electrification has become the default in dense urban areas. We see in some EU jurisdictions already, preferential driving times for electric trucks.

Tailwind #2 Policy Support

Electrifying road freight delivers high societal value. We have estimated that each electric truck avoids around 466 tonnes of CO₂e per year. With a conservative CO2 breakeven point reached after just 68,000 kilometres (Scania LCA study), approximately 14 percent of the vehicle’s lifetime travel. The long-run climate benefit is substantial. When we apply a social cost of carbon to this externality, we estimate that the total impact market exceeds €410 billion each year.

Policymakers are beginning to recognise this. In recent years, support has combined incentives for electrification with penalties for continued combustion. On the incentive side, the EU’s Clean Vehicles Directive mandates growing quotas for zero-emission vehicles in public fleets. In Germany, subsidies have covered up to 80 percent of the incremental cost of electric trucks. The UK has introduced purchase support schemes to reduce upfront CAPEX.

On the penalty side, the EU is introducing ETS2, a second emissions trading scheme that will apply to fuel combustion in road transport. Reporting starts in 2025, with full implementation set for 2027. Unlike ETS1, no free allowances will be provided. Fuel retailers will be responsible for compliance. Germany has already introduced a CO₂-based toll for trucks, creating an additional operating cost for diesel vehicles.

Another prominent penalty mechanism already in place in the EU is the CO2 emission limits placed on OEMs. From July 1st 2025 the sold vehicles emissions are accounted for and non-compliance can result in hefty fines. As a result, we expect to see a notable increase in new vehicle registrations this year in order to meet these targets.

That said, the direction of policy is not without friction. In the last year, lobbying by legacy automakers has slowed or diluted progress across several EU markets. The US may see reversals of federal vehicle emissions mandates. California’s Advanced Clean Cars II waiver faces legal uncertainty. In the UK, the phase-out date for new combustion vans has been pushed from 2030 to 2035, and ZEV sales mandates have been softened.

InfluenceMap, revealed that brands producing the lowest proportion of EVs are pushing hardest against progressive policies to cut emissions from road transport. The persistent strength of this lobby to limit change is a key uncertainty, and puts caution to the timing of this transition.

Our belief is that by addressing the fundamental economics of ownership of EVs, we can somewhat mitigate this risk, and that whilst politics may wobble, the direction of decarbonisation remains too valuable to society to reverse.

Barriers to scaling EV trucks

The core barrier to scaling electric HGVs is economic. Operators make decisions based on total cost of ownership, and in most cases today, electric trucks are still more expensive to run than diesel or HVO alternatives. We believe two factors explain most of that gap: high upfront and high charging costs. We are also seeing an issue that intersects costs and operational complexity, that is the current lack of available charging and rest infrastructure for drivers. We will dissect these one-by-one.

Barrier #1: Vehicle CAPEX

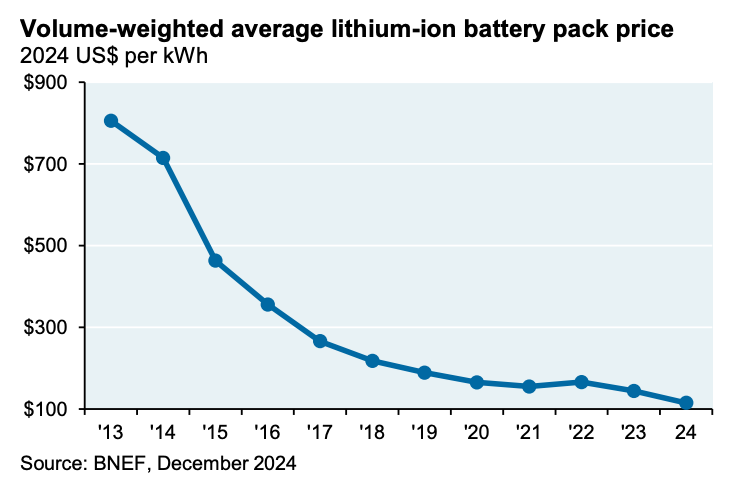

The lifetime cost of an electric truck is driven heavily by the upfront cost and batteries make up 40 to 50 percent of the purchase price of a new electric truck (BBC, ITDP). Operators can expect to pay 2-3x the diesel price on a new EV tractor.

However, we’re already seeing progress in addressing this barrier as battery costs continue to plummet. And we expect that along with this, the scaling of BEV production capacities by the major OEMs and competition from China, will continue to drive down the vehicle price.

For context, the Lithium ion battery pack prices continue to decline after a temporary spike in 2022, which is driving the declines across the industry.

Lithium iron phosphate (LFP) chemistry is now a prominent technology used in the truck segment (e.g. Daimler). A BNEF analysis suggested that battery cells manufactured in China cost roughly half as much as those produced elsewhere. Of course this is perhaps unfair given they utilise a 2023 global average. Nevertheless, this helps explain the cost advantage of Chinese OEMs.

We expect that large fleet operators will increasingly overcome this barrier. They can absorb higher upfront costs and amortise them over the vehicle’s lifetime, given the anticipated lower charging costs. But the road freight market is fragmented. A large share of volume, estimated to be over 50 percent, is handled by SMEs, often as subcontractors of the large operators. These operators often lack access to low-cost capital and face high financing costs due to residual value uncertainty. Banks are struggling to underwrite electric trucks confidently, and compensate by increasing interest rates. That cost is a real constraint on adoption.

Barrier #2 Charging cost

The second major driver of total cost of ownership is energy. The difference between affordable and unaffordable charging can make or break the economics of electric trucks.

The below McKinsey total cost of ownership analysis shows that public charging, when used inefficiently, makes BEVs more expensive than diesel trucks. But if charging infrastructure is shared, highly utilised and procures energy predictably, electric trucks can undercut diesel on cost. The key variable is utilisation, jumping from 10 percent to over 40 percent fundamentally shifts the cost structure.

Today, charging infrastructure is still early. Public networks are sparse, especially for long-haul routes, and operators face high energy prices. CPOs struggle to plan demand, access affordable energy, and recover capital. This creates a feedback loop: high prices deter operators, low demand weakens business models.

A large consumer goods company who has started to introduce EV HGVs to their fleet said their breakeven charging costs are around £20-22p / kWh, but we’re seeing public charging much higher than this, often in the £70-80p / kWh.

We believe this is solvable. The opportunity lies in connecting vehicle dispatch with energy procurement. If logistics operators and CPOs can coordinate in real time (on routing, charging, and energy use) utilisation improves, cost drops, and both sides win. Battery integration adds a further layer of optimisation. Truck batteries can serve as flexible energy assets, enabling arbitrage, peak shaving and grid services. If fully deployed, the EU truck fleet could eventually offer >2TWh of flexible storage, more than half of daily EU electricity consumption (Ember, European Electricity Review 2025). A quick estimate puts current E-trucks at 0.079% of EU daily consumption, in equivalent battery capacity. We have some way to go.

But for now, poor utilisation keeps costs high, and limits the case for both fleets and infrastructure investors.

Barrier #3 Charging availability and certainty

Charging infrastructure for heavy-duty trucks remains sparse, especially for long-haul routes. While depot charging will cover most short- and medium-haul needs, long-distance freight requires reliable public infrastructure. That infrastructure does not yet exist at the scale or quality required.

Grid connection is the first constraint. High-powered semi-public charging hubs have a high power requirement in order to offer fast charging for 600kWh+ batteries. We anticipate this being a material bottleneck in some regions across the EU, not least due to competition with the rapid growth in data centers also requiring high power grid connection.

Meanwhile, rest infrastructure for drivers is already under strain. Overnight parking capacity is insufficient. Of the 75,000 trucks parked each night in the EU, only around 51,000 designated spaces exist. Charging adds to that pressure. Once plugged in, trucks cannot be moved. This locks up space and demands a one-to-one pairing of charging point and parking spot. Midday charging during mandated breaks adds another layer of congestion.

Driver satisfaction is also a factor. Surveys, such as the NEFTON project, show high levels of dissatisfaction with rest area quality. Over 40 percent of drivers report substandard conditions, including lack of toilets, showers, and safe, available parking.

The challenge and opportunity go hand in hand. Well-designed charging hubs that integrate rest facilities can solve both problems. Long stops allow for slower, cheaper charging. Purpose-built sites that address driver needs can unlock better energy economics, higher utilisation and safer, more reliable operations. Electrification gives us a reason to rebuild the system. The economics of these new models of rest and charging remain somewhat unclear, and rely on high penetration of EVs across the major trade routes. This will be a play on market timing.

What about Autonomous?

Autonomous trucking has the potential to be a major unlock, not as a replacement for electrification, but as a multiplier.

Removing or reducing the need for a human driver transforms the cost structure of freight. Labour is a major operating expense, and driver rest requirements place hard limits on utilisation. Autonomy removes those constraints. Trucks can run closer to 24 hours per day. Charging schedules can be optimised for grid conditions, price signals and route efficiency. Battery usage can be planned with far more precision than in a human-driven system.

There are also phased approaches being explored. Some models retain human drivers for urban or complex segments, or bring in drivers remotely for the last few miles. This could make early deployment feasible in long-haul or highway-dominant corridors.

OEMs appear bullish. Many have active investments in autonomous systems and see autonomy as strategically important to future vehicle platforms. But there is still meaningful scepticism from operators, especially those with deep logistics experience. Some see autonomy as perpetually ten years away. Others point to the regulatory and safety hurdles that remain unresolved.

We believe the timeline is uncertain, but the direction is clear. The commercial case for autonomy is strong, and when combined with electrification, even stronger. It reinforces the case for better route planning, energy optimisation and system-level orchestration. The trucks may take longer to arrive than promised, but the enabling software and infrastructure can start creating value well before then.

Autonomy also raises the question of non-truck vehicles. In last-mile delivery, autonomous systems are already gaining traction. Companies like Zipline, Einride and Avride are building drone and small-format autonomous delivery platforms that can operate at lower regulatory thresholds. These systems are well-suited to dense urban areas and short-range logistics, where payload requirements are lighter and route complexity is higher.

We see this playing out primarily in last-mile and intra-urban delivery, rather than displacing long-haul trucking. It fills the gap between distribution hubs and end-customers, not between factories and warehouses.

This segment is also emerging as an InfraTech opportunity. These platforms combine capital-intensive deployment with defensible technology, but without depending on moonshot deeptech.

Problems We’re Excited About

We believe some of the most impactful companies of the coming decades will emerge by tackling one or more of the following problem areas. We're eager to meet founders building solutions here.

1. Boosting Charging Infrastructure Utilisation for CPOs

Charging infrastructure operators currently face a catch 22: carriers are slow to adopt EVs due to high charging costs, yet these costs remain high because utilisation is low.

Unlocking guaranteed demand can break this cycle. With predictable volume, operators can lower prices, attracting more fleets. This effect compounds when charging infrastructure is managed across warehouses, depots, and public nodes as part of an integrated network. High-utilisation hubs can offer better pricing, which attracts more users, reinforcing the system.

This is the foundation for a network-effect-driven business that aligns incentives across stakeholders.

2. Integrated Route Planning and Energy Management for Carriers

Switching to electric freight is daunting. Range anxiety, poor visibility into charging options, and infrastructure built for smaller vehicles all contribute to uncertainty.

Integrating charging data into route planning can smooth this transition. Carriers benefit from real-time visibility into charging locations, battery range, and route optimisation. Layering on intelligent energy management, like time-of-day charging or grid integration at depot level, opens the door to reduced costs and greater predictability.

There’s also long-term potential in connecting vehicle batteries to the grid to provide energy flexibility and unlock pricing advantages.

3. Developing Charging Sites at Scale

Europe’s long-haul freight corridors aren’t ready for mass electrification. There’s a shortage of charging infrastructure for large trucks, and an even bigger gap in suitable rest areas for drivers.

Combining electrification infrastructure with rest facilities isn’t just convenient, it's strategic. Long stops enable cheaper, slower charging, and drivers benefit from reliable, well-equipped sites. This opportunity spans both physical infrastructure and software to optimise site use, demand management, and energy distribution.

4. EV-Native Full-Stack Logistics Operators

Transitioning a legacy fleet to electric is complex: new vehicle procurement, depot upgrades, route redesign, driver retraining, and exposure to charging uncertainty.

Instead of retrofitting old models, there's an opening to build logistics operators from the ground up fully electric, digitally native, and built to scale with the EV ecosystem. These players can own their own charging footprint, tailor operations to EV-specific constraints, and tap into optimisation benefits as route density increases.

Done right, these operators gain structural advantages over time through superior infrastructure access and operating efficiency.

5. Access to Trucks for SMEs

Small and medium carriers form the backbone of the European road freight sector, handling more than half of the total volume. Yet many of them can’t afford the upfront cost of switching to electric.

Even when EVs make sense on a total cost of ownership basis, financing remains a hurdle. Banks are wary of underwriting loans due to uncertainty around residual values, leading to higher interest rates that deter adoption.

We’re interested in solutions that de-risk EV financing for this segment be it through residual value insurance, usage-based finance models, or better asset tracking.

The Market Map

The market map below captures a snapshot of the current ecosystem: from CPOs, to disruptor OEMs and full-stack logistics operators. Who are we missing?

If you’re building in this space, we’d love to hear from you! Reach out on albert@revent.vc